Sat Mar 23, 2024 11:33 pm by globalturbo

Sat Mar 23, 2024 11:33 pm by globalturbo

New U.S. Currency Already in Our Money Supply

By Cosmic Convergence Research Group -

Jul 31, 2016

By Anonymous Patriots

For those of you that are stressing about the collapse of the U.S. dollar and the Federal Reserve, please take faith that initial measures have been taken to insure a not-so-hard landing when the Federal Reserve Note will be retired out of circulation, being replaced by notes printed and backed solely by the U.S. Treasury. If you have been putting your money under the mattress for the last few years, you will want to take the time to read this article so that you can replace the old fiat currency of the Federal Reserve Note (FRN) with new currency. We believe that those who do not start taking action will find in the near future that their fiat currency is unredeemable. This is particularly true of the billions of dollars that are held in cash outside of the United States, most of which will not be redeemable once the transition is made.

As our readers know, our articles can be a bit lengthy, but we like to fully educate you on our topics so that you can take the message and disseminate to your constituency in a manner that will resonate with them. Not everyone will need to know all the details, but for those reading this article, you are at the top level of the underground information pyramid for the New Fourth Estate and will need to know background and strategies for going forward.

In this article, you will learn:

First, we are making the assumption that the readers of this article are fully aware of the history and state of the Federal Reserve System and its unabashed money-printing operations in flooding the global markets with fiat currency. We also assume that you are knowledgeable about why and how the U.S. transitioned off the gold standard and why going back on it is critical for our economic future. Many people who will read this article will be aware of the constant attention Ron and Rand Paul have given this issue from auditing the Federal Reserve to seeding a movement to begin Fedexit.

In this bill above, we have the standard $100 before the blue security strip and other features were added. In the center is a picture of Benjamin Franklin, the only face on U.S. currency besides Alexander Hamilton, who was not a U.S. president. On the left side of the bill, you will find the words “Federal Reserve Note” and see the seal for the private corporation United States Federal Reserve System. On the right side, you find the words “The United States of America” and a seal with the same.

Pay close attention to the statement “This note is legal tender for all debts, public and private.” This is on the left side of the bill underneath the Federal Reserve seal.

Examine the new one-hundred-dollar bill.

Although this series was issued just after the 2008 financial crisis, it was not released into public circulation until 2013.

We were told that it had special security features so that it would not be easy to counterfeit. We see that Benjamin Franklin’s image is no longer encircled and has shifted left of the fold line.

If you are holding a new $100 bill, fold the bill in half where the two ends are exactly aligned with each other. You will notice that the blue 3-D security ribbon with images of bells and 100s is on the right side of the bill. Note that the security strip is not in the exact center of the folded bill, but just to the outside of the fold.

You will also notice a color-shifting bell inside a copper inkwell on the front of the note. The bell shifts in color from copper to green in an effect that makes the bell seem to appear and disappear in the inkwell.

What is really remarkable about the new bill is all the gold color and shimmer on the right side of the bill, which is conspicuously absent on the left side of the bill.

On the left side of the folded bill, you will see that Franklin is pictured, along with the Federal Reserve statement and emblem with signatures. Of course, Tim Geithner’s signature would remain on the Fed side of the bill.

But what you may have missed is where the phrase “This note is legal tender for all debts, public and private” is located. It is now on the right side of the bill.

The two halves of the bills look like two entirely different notes! On the left side, we have the old FRN which will be faded out just as the old $100 bills are being destroyed now and replaced by the hybrid FRN-USTN. On the right side we have the new currency hiding in plain sight. It is the right side of the $100 bill that is now “legal tender for all debts, public and private.” This statement is no longer on the FRN side of the bill.

Notice all of the gold on the right side of the bill—gold writing, feather pens, ink wells, numbers, liberty bells. This is the side of the note that seems to say “backed by gold.” Also notice the huge gold lettering on the number 100 on the back of the bill. It seems to scream gold, gold, and more gold.

The right side of the bill also has other hidden-in-plain sight messages about the new USTN currency. The pen and ink well remind us that We the People, or as it is written on the right side of the note “July 4, 1776, States of America” not “The United States of America” can eliminate the Federal Reserve or our existing government any time we like with the will of the people and the “stroke of the pen.”

Indeed, the opening words from the Declaration of Independence are written in gold on the right side of the bill under the golden feather and gold ink well with liberty bell. Not all of the words are legible, and some seem implied as they are hidden under images, but the passage clearly begins and ends with the phrases in this historic proclamation:

“When in the Course of human events, it becomes necessary for one people to dissolve the political bands which have connected them with another, and to assume among the powers of the earth, the separate and equal station to which the Laws of Nature and of Nature’s God entitle them, a decent respect to the opinions of mankind requires that they should declare the causes which impel them to the separation.

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.–That to secure these rights, Governments are instituted among Men, deriving their just powers from the consent of the governed, –That whenever any Form of Government becomes destructive of these ends, it is the Right of the People to alter or to abolish it, and to institute new Government, laying its foundation on such principles and organizing its powers in such form, as to them shall seem most likely to effect their Safety and Happiness. Prudence, indeed, will dictate that Governments long established should not be changed for light and transient causes; and accordingly all experience hath shewn, that mankind are more disposed to suffer, while evils are sufferable, than to right themselves by abolishing the forms to which they are accustomed. But when a long train of abuses and usurpations, pursuing invariably the same Object.”

As you hold the folded new $100 bill in your hand, it is though it has been designed to be a redeemable “coupon” where one would tear or cut the left side off the bill, discarding it for the worthless paper it has become. There is even room to cut the bill in half without damaging the 3-D security strip.

This leaves the right side, ornate with gold, to be used as transitional legal tender until a new currency can be printed and circulated. Think “out of the box” and you will see that there is no rule about what the dimensions of a bill should be, other than vending machines that require a certain size of a bill. We could certainly exchange this new currency for goods and services. Even though it would be one-half the size of the old bill, it would be far more valuable. By eliminating the left side of the bill, the Federal Reserve side, we will be discarding nothing but the yoke of financial slavery.

We are not suggesting or advocating destruction of currency. When the system is ready to be collapsed, it will be done like the controlled demolition of World Trade Center building #7. American citizens will be given notice and will be instructed how to exit the old Federal Reserve currency system. But in the meantime, Patriots may want to switch out their old FRNs for the hybrid note.

Once the old pre-2009 series $100 bills are out of circulation and the left side of the new $100 bill have been deemed worthless, we are left with $100 bill currencies that have been circulated post 2013. If you are a foreign nation or illicit operation, hoarding great quantities of U.S. dollars, you are more than likely holding OLD U.S. dollars. It is going to be very difficult to exchange your old fiat currency for the new gold-backed U. S. currency, especially with the new banking regulations that only permit limited cash transactions every day and have limits of how much cash can be brought in to the U.S. at any one time.

If you are a patriot, with a few thousand dollars put away in your home safe, you might consider taking the old $100 bills out of safekeeping and spending them while they are still good. If you want to hold cash, you might consider only holding blue stripe currency.

Once the play is made to dump the FRN, those who have been holding money legally should not have any problems with cash issues. Our domestic bank accounts should also be good as the digital figures in your account would be backed by the Treasury.

Entities, both foreign and domestic, or bank accounts outside of the U.S. system (such as off shore), especially agents holding large quantities of cash, may find their FRNs have no value once the fiat system collapses. This is a strategic way of eliminating currency from an over-bloated cash bubble market. One way or another agents and entities will have to suffer from the collapse of the fiat FRN.

By sneaking in the new currency on the back (or side) of the old currency, we are soft landing this behemoth Hindenburg fiscal balloon before it traps all of us in its fiery flames. By nullifying the old FRNs and accounts held digitally outside of the U.S. banking system, we would not have to face extreme inflation or the total collapse of the dollar. Trillions of dollars would be wiped out of the global market, giving our new gold-back dollars and digits value again.

We cannot comment if other currencies in other countries have undergone these changes. If you are not in the U.S., you might pay attention to your larger bills and see if they have been altered in a similar fashion.

Franklin was a diplomat to England and France and his wisdom in fiat currency manipulation fared well in the Colonies while England’s commerce was stagnant due to currency shortage. The Tea Tax, Stamp Tax and other English intrusions into Colonial commercial matters led to a rebellion that was also a battle against Central Banking based upon gold/silver backed fiat currency. Franklin could see that repaying the interest debt on the issue of fiat currency, which would continually need new notes issued to match the need of commerce, would never be able to be paid and the system would enslave those caught in its trap.

Franklin’s good friend Thomas Jefferson said: “I believe that banking institutions are more dangerous to our liberties than standing armies. If the American people ever allow private banks to control the issue of their currency, first by inflation then by deflation, the banks and the corporations that will grow up around them [the banks] will deprive the people of all property until their children wake up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” (From a 1802 letter to Secretary of the Treasury Albert Gallatin)

The American Revolution was not only a political and Freemasonic rebellion (Franklin was the top Freemason in Pennsylvania), but it was also a “banking” rebellion that tried to stop England from enslaving the Colonies through hard metal backed fiat currency or the attempt to create a National Land-Backed Bank that would be owned by England. This was simply an English attempt to steal all of the real estate in the Colonies. These attempts have not stopped even to this day and essentially the Government Self- Regulated Mortgage Electronic Registration Systems, Inc. company, or what some call the Mortgage Mafia, is still trying to steal land from Americans with the help of “warlord” bankers.

Franklin would be proud that his picture on the bill honors his own ingenious ways of defeating counterfeiting of paper currency. He developed a method of imprinting plant substance into the process that was very hard to duplicate. The watermarked picture of Franklin on the “Blue” $100 dollar bill is there as a counter measure for counterfeiting. You can only see the picture when you hold it up to the light.

So the overt picture of Franklin – the king of non-gold fiat currency remains on the side that will become worthless paper that is only backed up by debt at the Federal Reserve System who issues these fraudulent Federal Reserve Notes. This debt was created by a private corporation (FRS) through bad management and should go bankrupt while the gold side of the Blue Bill represents a Treasury Note that is backed up by gold (and silver) just like the new IMF Reserve Currencies of Russia and China. Once we drop our fictitious Federal Reserve Debt, we can compete again with respect in world currency markets.

Money creation via quantitative easing only leads to inflation; bailing out banks only puts more money into the market which also leads to inflation. We have reached the point now where our money holds such little value that the Federal Reserve can’t even give itself income (interest rates) off the money it prints. This is why Janet Yellen can’t raise rates.

The Federal Reserve System was created by the Congress to provide the nation with a safer, more flexible, and more stable monetary and financial system. If it were doing its job, it would “call in” the oversupply of money by increasing interest rates. But they won’t do this because their globalist big-corporate-buddies, who they really serve, would be in a world of hurt. Their cost of business would go up and so would consumer prices. That, in turn, would slow down consumer spending and cause industry to stall. Banks would also be impacted in this call-back-the-money strategy as fewer loans would be made as consumers might not buy houses and cars, and businesses would not need commercial loans to expand their operations since consumer spending would be reduced.

If the Fed had been doing its job, it would not have printed money at a pace to create an oversupply of money in the global market. A limited audit of the Fed after the 2008 financial crisis revealed that between 2007 and 2008 the Federal Reserve loaned over $16 trillion — more than four times the annual budget of the United States — to foreign central banks and globalist private companies.

There are two ways out of the Ponzi scheme of all time: a total collapse or a controlled demolition.

When we pick up the pieces of the failed fiat system, we will be smarter and wiser and choose a better course of running our economy:

Why this is of particular interest in this article is that as the properties were paid off, we would ask the bank for our property titles. We kept being told that “we don’t issue property titles anymore” or “the proof of your ownership is now established with your local property tax authorities.” But this was odd since we have auto titles in our possession. Friends with boats and mobile homes have paper titles.

So what happened to property titles? We paid off our home and buildings—but do we really own them when we don’t have a paper legal title? What did the banks do with the original title and why don’t they return them to us now that the property is paid-in-full? Do you have the title to your residence or have you ever seen it? If you closed on a home since 2008 have you seen any paper titles at closing? Why aren’t title companies and banks concerned about paper titles anymore?

We were curious what would image would show if we folded a new $100 bill in the same manner. This is what we found, taken from the 2009 series of the new bill, which predates the event that we will describe below, but seems to be a prophetic warning nonetheless:

We see what seems to be a rush of water down a street, from an open source of water, into an urban area. This is what we began to search on the internet. Had there been any floods in urban areas that might have currency consequences?

The DTCC processes the underwriting of stock and bond offerings for all transactions on the New York Stock Exchange and electronically registers securities and ensures that dividend payments are accurate. It also manages transactions and payments in equities and fixed income and guarantees that trades clear. Purchases and sales are mainly handled through electronic book entry, with the securities registered in the name of DTCC unit Cede & Co. The DTCC is owned by its member banks, brokers, mutual funds and other financial institutions.

The “Unfortunate and Unpredictable” destruction of $40 Trillion in Stocks and Bonds must have come as a shock seeing that a fifth grader wouldn’t house the largest depository of “paper” stocks and bonds in a vault below sea level and then, forget to close the door. That’s right, the vault was waterproof, but someone forgot to close the door on the way out after they heard the largest hurricane to ever hit Manhattan was on the way. But that is only topped by the fact that after the flood drained, a fire somehow burnt the contents of the vault. And then, another flood somehow filled the vault again leaving a mess that DTCC says may never be cleared up.

From the site of the DTCC, September 1, 2012

Targeting Paper

DTCC Calls for Full Dematerialization

DTCC’s dematerialization plan focuses on three primary areas in physical processing: traditional physical transactions, new issues and existing inventory in the vaults of The Depository Trust Company (DTC). To target these areas, DTC will:

As of September 2014, DTCC had not replaced the damaged stock certificates and had laws suites filed against it. There were also many thousands of FBI and other documents also stored in this “depository.” DTCC was not worried at all about the loss because most the of the stocks and bonds were owned by their sister partner, Cede & Co. And as we can see in their Targeting Paper above, DTCC was hoping to “dematerialize” the Cede & Co stock and bonds…then OOPS!…Someone just happened to leave the vault door open for Hurricane Sandy.

It is worth taking a moment here and delving into the mystery company DTCC and its partner in crime, Cede & Company.

DTCC’s depository provides custody and asset servicing for more than 3.6 million securities issues from the United States and 121 other countries and territories, valued at US $36.5 trillion. In 2010, DTCC settled nearly US $1.66 quadrillion in securities transactions in 2012.

DTCC is about 34% owned by the New York Stock Exchange on behalf of its members. It is a limited purpose trust company and is a unit of the Federal Reserve.

Since the DTC is a banking trust company, it can’t hold the certificates in its name wither…..so the DTCC transfers the certificates to its own private holding company or nominee name. The DTCC’s private holding company or street name, is shown as either “CEDE and Company”, “Cede Company” or “Cede & Co.” After this transactional process, you, the so-called purchaser of the stocks, have no real, no actual, no legal claim over these stocks, certificates, or bonds.

Or, as one stockbroker said about the DTCC and ownership of stock: “Nobody owns stock. What you own is an entitlement to stock held for you by your broker. But your broker doesn’t own the stock either. What your broker owns is an entitlement to stock held for it by Cede & Co., which is a nominee of the Depository Trust Company, which is a company that is in the business of owning everyone’s stock for them. If I sell stock to you, I don’t have to courier over a paper share certificate, or call up the company and have it change its shareholder register. Our brokers just change some electronic entries at their DTC accounts and everything is cool.”

For those readers who made it so far, don’t think that you are an exception. Continue to read on:

When the Mortgage Electronic Registration Systems, Inc. was created, it was intended to serve as a nominee for real estate transactions in a way strongly analogous to how Cede & Co. serves as the nominee owner of record (i.e., the “street name” owner) for all securities held in trust by the Depository Trust & Clearing Corporation. In the late 1960s and early 1970s, the American securities industry was drowning in paper because of the sheer complexity of physically exchanging thousands of stock certificates every day. By “immobilizing” physical stock certificates and later replacing them altogether with book entries, DTCC enabled the development of the modern computerized securities industry.

The MERS system eRegistry is a system of record that identifies the owner (Controller) and custodian (Location) for registered eNotes. Built by MERSCORP Holdings, Inc. with the endorsement of the Mortgage Bankers Association (MBA) and launched in 2004. Both Fannie Mae and Freddie Mac require the registration of eNotes on the MERS system eRegistry before they are eligible for purchase.

As mortgage-backed securities grew in volume during the 1980s, it became self-evident that a similar mechanism was needed for the mortgages placed into those securities. MERS fixed this problem in that most standard loan documents were changed to name MERS as the nominal beneficiary or mortgagee of record. This enabled lenders and investors to transfer mortgages without recording assignments in local recorders’ offices and, in turn, avoided having to pay recording fees.

Ideally, assuming a loan is properly paid back on time, a MERS loan needs only two documents to be recorded:

1) the original mortgage or deed of trust naming Mortgage Electronic Registration Systems, Inc., and a reconveyance of the mortgage or

2) deed of trust back to the borrower (thus merging legal and equitable title).

If all entities along the way are MERSCORP Holdings, Inc. members, then all intermediate transfers between those points are tracked only on the MERS system, and the entity who holds the loan at the end merely records the reconveyance as an agent for MERSCORP Holdings, Inc. (Notice how MERS is both (1) an agent for the original lender, and then (2) the final lender acts as an agent for MERSCORP Holdings, Inc.; this is why MERS’ critics frequently attack it as “two-faced.”)

Some of the illegal activities of MERS named in the many law suits against it include:

MERS’s officers often issue assignments without verifying the underlying information, which has resulted in incorrect or fraudulent transfers.

Simultaneously claim to be the mortgagee and the nominee/agent of the lender or trustee.

Harmful effect on the integrity and transparency of public recording and tax avoidance.

Its nominal ownership of millions of home loans poses a disastrous risk for mortgage investors should Mortgage Electronic Registration Systems, Inc. ever declare bankruptcy.

MERS was used by the Wall Street Banks to avoid paying county recorder fees and real estate transfer tax fees.

Using a long list of names who are known “robo-signers.”

MERS is a shell company with no employees, owned by the giant banks.

MERS is a tax and fee-avoiding opportunity.

MERS has all but replaced the nation’s public land ownership records.

MERS placed many undiscovered and no document mortgages in circulation.

The bundling and sale of mortgages and claims of title can make it very difficult to know who owes what to whom.

For the first time in the nation’s history, there is no longer an authoritative, public record of who owns land in each county.

There is an unbelievable scandal in the making that threatens to subvert our four-century-old method for guaranteeing a fundamental building block of the American republic—property ownership.

Created in 1995 by the country’s biggest banks, MERS quietly took control of and privatized mortgage record-keeping across the country and, in the span of a few years, scrambled America’s private property ownership records to the point where no one could figure out who owns what.

MERS was a tool used by America’s top financial institutions to pump up the real estate market.

Mortgage-backed securities, robo-signers, lightning quick foreclosures, subprime mortgages and just about everything else that went into feeding the biggest real estate bubble in U.S. history could not function without help from MERS.

MERS was created to help the industry push its latest money-maker: mortgage-backed securities, a Wall Street financial scam that dressed up the most toxic, guaranteed-to-fail loans as Grade A investment vehicles that could be sold to suckers looking for an easy gain.

The whole purpose of MERS is to allow “servicers” to pretend as if they are someone else: the “owners” of the mortgage, or the real parties in interest.

MERS artifice and enterprise evolved into an “ultra-fictitious” entity, which can also be understood as a “meta-corporation.”

The average consumer, or even legal professional, can never determine who or what was or is ultimately receiving the benefits of any mortgage payments. The conspirators set about to confuse everyone as to who owned what. The use of MERS as a generic placeholder for the real owner of a mortgage was a crucial component of the entire securitization machine. The entire scheme was predicated upon the fraudulent designation of MERS as the ‘beneficiary’ under millions of deeds of trust.

Before MERS, it would not have been possible for mortgages with no market value to be sold at a profit or collateralized and sold as mortgage-backed securities. Before MERS, it would not have been possible for the Defendant banks and AIG to conceal from government regulators the extent of risk of financial losses those entities faced from the predatory origination of residential loans and the fraudulent re-sale and securitization of those otherwise non-marketable loans.

From 1997—the year MERS went online—to 2005, mortgage fraud reports increased by 1,411 percent. MERS saved the banking industry—and cost municipal governments—tens of billions of dollars by allowing lenders to avoid paying county filing fees. MERS extracted at minimum around $30 billion from cash-strapped local governments.

MERS also has almost no paid employees and does not keep any records or minutes of corporate meetings. When pressed to explain the inner workings of the organization, its executives evaded questions, feigned ignorance.

In California, the suit against MERS could cost the company somewhere between $60 to $120 billion in damages and penalties.

Almost every participating major bank in MERS has been charged for mortgage fraud and paid fines in the billions.

The resulting global bank windfall, in stark contrast to individuals and companies both domestic and foreign, who lost big-time on these credit default swaps, and were forced to search out and attempt foreclosure on at-risk properties (whether in default or not) in order to recoup their losses and stay in the game.

The huge derivatives bubble created by the banks has created over 70 million MERS tainted properties in the US alone.

After deregulation (the Glass-Steagall repeal) the mortgage note, and the lien document were allowed to be separated. The seller would keep the lien and the note was sold to the bank for consideration which the bank then sold into a Wall Street derivative pool. There it was leveraged and resold over and over again. There are literally hundreds of court cases from 17th century English case law to today’s US Supreme Court that have ruled this practice of unrecorded title transfer as predatory and unlawful.

The Note is the signed negotiable instrument, you executed to obtain the money you borrowed. For this reason payment is due only to the lawful holder of this NOTE or to an agent who can prove he lawfully represents the owner of the actual Note and not just a copy of it. By the same token, the lien holder, has no claim to the property without possession of the actual Note.

Any mortgage company that demands payment on any property, cannot secure and lawfully receive payment nor can they foreclose and lawfully take the property with merely a copy of the mortgage Note. Any foreclosure without both the Lien and the original Note is theft.

The solution is to hold the mortgage bankers’ feet to the fire. Never let them take your property — possession is 9/10ths of the LAW. Arm yourself with the facts and make them prove their ownership in court. If they can’t prove they are the mortgage owner by producing absolute proof of the legally obtained original Note signed by you in blue ink, don’t pay them a penny and don’t let them take your property. They must be the legal holder of your Note and Lien to lawfully do so.

The move to digitalize all stocks and mortgages is similar to going from gold backed fiat currency to currency backed by digital impulses in the servers of meta-corporations which are monopolies.

Would you be surprised to know that the same company that owns the New York Stock Exchange also owns the Chicago Mercantile Exchange and most other national and international exchanges? Surely you would not be surprised to find out that the same transnational private corporation also owns DTCC and Cede & Co. and MERS. It sounds like checkmate, doesn’t it? But in coming articles we will reveal the name of this “most powerful” corporation and the evil web it spins.

They also included a very important message to all of us on the new currency. We The People, by the stroke of a pen and the will of the people, can determine the outcome of this war. Let Patriots around the country consider the following actions:

Until then, don’t take any wooden nickels, old Federal Reserve Notes and remember to demand paper copies of all titles, notes, liens, stocks and bonds. Until then, keep holding on to those Blue bills. And when we have a favorable political situation in Washington, we must demand, by Constitutional Amendment or rock-solid legislation, the complete cessation of the DIGITALIZATION of our money, stocks and bonds, and LAND of the citizenry.

Thanks to: http://www.cosmiconvergence.com

By Cosmic Convergence Research Group -

Jul 31, 2016

By Anonymous Patriots

For those of you that are stressing about the collapse of the U.S. dollar and the Federal Reserve, please take faith that initial measures have been taken to insure a not-so-hard landing when the Federal Reserve Note will be retired out of circulation, being replaced by notes printed and backed solely by the U.S. Treasury. If you have been putting your money under the mattress for the last few years, you will want to take the time to read this article so that you can replace the old fiat currency of the Federal Reserve Note (FRN) with new currency. We believe that those who do not start taking action will find in the near future that their fiat currency is unredeemable. This is particularly true of the billions of dollars that are held in cash outside of the United States, most of which will not be redeemable once the transition is made.

As our readers know, our articles can be a bit lengthy, but we like to fully educate you on our topics so that you can take the message and disseminate to your constituency in a manner that will resonate with them. Not everyone will need to know all the details, but for those reading this article, you are at the top level of the underground information pyramid for the New Fourth Estate and will need to know background and strategies for going forward.

In this article, you will learn:

- How the 2009 $100 bill series is a hybrid of the old FRN and the new USTN (US Treasury Note);

- How the old $50 FRN has been replaced with a new USTN $50 bill;

- How to protect your cash stash if you are still holding old FRNs;

- How Benjamin Franklin created fiat currency and why his image will be destroyed on the $100 FRN as a symbol of the We the People choosing to govern ourselves again and eliminating Globalists from our banking and government systems;

- How the new USTN is backed by the gold-silver standard;

- A hidden symbol in the new USTN that explains how U.S. wealth was wiped out in 2009 with a flood-fire-flood on Water Street;

- Why you can’t get a title to your real estate once you have paid off your mortgage;

- How We the People are instrumental in completing the process of making the big switch;

- How our money supply will become a mixture of digital, paper, and metals in the near future as long as We the People wake up and see the writing on the $100 bill.

First, we are making the assumption that the readers of this article are fully aware of the history and state of the Federal Reserve System and its unabashed money-printing operations in flooding the global markets with fiat currency. We also assume that you are knowledgeable about why and how the U.S. transitioned off the gold standard and why going back on it is critical for our economic future. Many people who will read this article will be aware of the constant attention Ron and Rand Paul have given this issue from auditing the Federal Reserve to seeding a movement to begin Fedexit.

2009 $100 bill series is a hybrid of the old FRN and the new USTN

Here are two pictures. The top one is of the $100 bill prior to 2009 series. The bottom one is the “blue” one-hundred-dollar bill that was purported to be made for security purposes in a 2009 series. If you have an old and a new bill on hand, please hold and compare them as we walk through this explanation.In this bill above, we have the standard $100 before the blue security strip and other features were added. In the center is a picture of Benjamin Franklin, the only face on U.S. currency besides Alexander Hamilton, who was not a U.S. president. On the left side of the bill, you will find the words “Federal Reserve Note” and see the seal for the private corporation United States Federal Reserve System. On the right side, you find the words “The United States of America” and a seal with the same.

Pay close attention to the statement “This note is legal tender for all debts, public and private.” This is on the left side of the bill underneath the Federal Reserve seal.

Examine the new one-hundred-dollar bill.

Although this series was issued just after the 2008 financial crisis, it was not released into public circulation until 2013.

We were told that it had special security features so that it would not be easy to counterfeit. We see that Benjamin Franklin’s image is no longer encircled and has shifted left of the fold line.

If you are holding a new $100 bill, fold the bill in half where the two ends are exactly aligned with each other. You will notice that the blue 3-D security ribbon with images of bells and 100s is on the right side of the bill. Note that the security strip is not in the exact center of the folded bill, but just to the outside of the fold.

You will also notice a color-shifting bell inside a copper inkwell on the front of the note. The bell shifts in color from copper to green in an effect that makes the bell seem to appear and disappear in the inkwell.

What is really remarkable about the new bill is all the gold color and shimmer on the right side of the bill, which is conspicuously absent on the left side of the bill.

On the left side of the folded bill, you will see that Franklin is pictured, along with the Federal Reserve statement and emblem with signatures. Of course, Tim Geithner’s signature would remain on the Fed side of the bill.

But what you may have missed is where the phrase “This note is legal tender for all debts, public and private” is located. It is now on the right side of the bill.

The two halves of the bills look like two entirely different notes! On the left side, we have the old FRN which will be faded out just as the old $100 bills are being destroyed now and replaced by the hybrid FRN-USTN. On the right side we have the new currency hiding in plain sight. It is the right side of the $100 bill that is now “legal tender for all debts, public and private.” This statement is no longer on the FRN side of the bill.

Notice all of the gold on the right side of the bill—gold writing, feather pens, ink wells, numbers, liberty bells. This is the side of the note that seems to say “backed by gold.” Also notice the huge gold lettering on the number 100 on the back of the bill. It seems to scream gold, gold, and more gold.

The right side of the bill also has other hidden-in-plain sight messages about the new USTN currency. The pen and ink well remind us that We the People, or as it is written on the right side of the note “July 4, 1776, States of America” not “The United States of America” can eliminate the Federal Reserve or our existing government any time we like with the will of the people and the “stroke of the pen.”

Indeed, the opening words from the Declaration of Independence are written in gold on the right side of the bill under the golden feather and gold ink well with liberty bell. Not all of the words are legible, and some seem implied as they are hidden under images, but the passage clearly begins and ends with the phrases in this historic proclamation:

“When in the Course of human events, it becomes necessary for one people to dissolve the political bands which have connected them with another, and to assume among the powers of the earth, the separate and equal station to which the Laws of Nature and of Nature’s God entitle them, a decent respect to the opinions of mankind requires that they should declare the causes which impel them to the separation.

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.–That to secure these rights, Governments are instituted among Men, deriving their just powers from the consent of the governed, –That whenever any Form of Government becomes destructive of these ends, it is the Right of the People to alter or to abolish it, and to institute new Government, laying its foundation on such principles and organizing its powers in such form, as to them shall seem most likely to effect their Safety and Happiness. Prudence, indeed, will dictate that Governments long established should not be changed for light and transient causes; and accordingly all experience hath shewn, that mankind are more disposed to suffer, while evils are sufferable, than to right themselves by abolishing the forms to which they are accustomed. But when a long train of abuses and usurpations, pursuing invariably the same Object.”

As you hold the folded new $100 bill in your hand, it is though it has been designed to be a redeemable “coupon” where one would tear or cut the left side off the bill, discarding it for the worthless paper it has become. There is even room to cut the bill in half without damaging the 3-D security strip.

This leaves the right side, ornate with gold, to be used as transitional legal tender until a new currency can be printed and circulated. Think “out of the box” and you will see that there is no rule about what the dimensions of a bill should be, other than vending machines that require a certain size of a bill. We could certainly exchange this new currency for goods and services. Even though it would be one-half the size of the old bill, it would be far more valuable. By eliminating the left side of the bill, the Federal Reserve side, we will be discarding nothing but the yoke of financial slavery.

We are not suggesting or advocating destruction of currency. When the system is ready to be collapsed, it will be done like the controlled demolition of World Trade Center building #7. American citizens will be given notice and will be instructed how to exit the old Federal Reserve currency system. But in the meantime, Patriots may want to switch out their old FRNs for the hybrid note.

Why Was the $100 Bill Selected to be the Transition Currency?

The $100 bill is the second most common bill in circulation, behind the $1 bill. At the end of 2012, according to The Exchange, there were $863.1 billion in $100 bills (or 8.631 billion notes) compared to 10.3 billion $1 notes in circulation. But what is more interesting is that as more people lose faith in the government and big banks, the $100 bill has become the most popular note to hoard—here in the U.S. and overseas. It is estimated by many sources that the majority of $100 bills are probably being held overseas.Once the old pre-2009 series $100 bills are out of circulation and the left side of the new $100 bill have been deemed worthless, we are left with $100 bill currencies that have been circulated post 2013. If you are a foreign nation or illicit operation, hoarding great quantities of U.S. dollars, you are more than likely holding OLD U.S. dollars. It is going to be very difficult to exchange your old fiat currency for the new gold-backed U. S. currency, especially with the new banking regulations that only permit limited cash transactions every day and have limits of how much cash can be brought in to the U.S. at any one time.

If you are a patriot, with a few thousand dollars put away in your home safe, you might consider taking the old $100 bills out of safekeeping and spending them while they are still good. If you want to hold cash, you might consider only holding blue stripe currency.

Once the play is made to dump the FRN, those who have been holding money legally should not have any problems with cash issues. Our domestic bank accounts should also be good as the digital figures in your account would be backed by the Treasury.

Entities, both foreign and domestic, or bank accounts outside of the U.S. system (such as off shore), especially agents holding large quantities of cash, may find their FRNs have no value once the fiat system collapses. This is a strategic way of eliminating currency from an over-bloated cash bubble market. One way or another agents and entities will have to suffer from the collapse of the fiat FRN.

By sneaking in the new currency on the back (or side) of the old currency, we are soft landing this behemoth Hindenburg fiscal balloon before it traps all of us in its fiery flames. By nullifying the old FRNs and accounts held digitally outside of the U.S. banking system, we would not have to face extreme inflation or the total collapse of the dollar. Trillions of dollars would be wiped out of the global market, giving our new gold-back dollars and digits value again.

What About Other Denominations and Other Currencies?

The U.S. fifty-dollar FRN was also changed. There is now color on the right side—both the red flag waving lines as well as a gold number fifty and a silver star. Holding the fifty to light you will see a narrow security thread running vertically to the right of Grant’s portrait. In ultraviolet light this thread appears gold (or yellow). It seems that the same play is in place for the fifty-dollar note, accept it has not undergone the drastic changes that the $100 bill has.We cannot comment if other currencies in other countries have undergone these changes. If you are not in the U.S., you might pay attention to your larger bills and see if they have been altered in a similar fashion.

Good-bye Benjamin Franklin

Benjamin Franklin was probably chosen for the $100 bill because of his well-known printing of Colonial fiat currency in Pennsylvania and throughout the other 12 Colonies. He was a major spokesman for land-backed fiat currency that could be adjusted by the issuer who held land notes and mortgages. Gold and silver fiat currency drained the Colonies of the currency that drove commerce as hard metal was paid to England and Europe for the commodities the Colonies purchased.Franklin was a diplomat to England and France and his wisdom in fiat currency manipulation fared well in the Colonies while England’s commerce was stagnant due to currency shortage. The Tea Tax, Stamp Tax and other English intrusions into Colonial commercial matters led to a rebellion that was also a battle against Central Banking based upon gold/silver backed fiat currency. Franklin could see that repaying the interest debt on the issue of fiat currency, which would continually need new notes issued to match the need of commerce, would never be able to be paid and the system would enslave those caught in its trap.

Franklin’s good friend Thomas Jefferson said: “I believe that banking institutions are more dangerous to our liberties than standing armies. If the American people ever allow private banks to control the issue of their currency, first by inflation then by deflation, the banks and the corporations that will grow up around them [the banks] will deprive the people of all property until their children wake up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” (From a 1802 letter to Secretary of the Treasury Albert Gallatin)

The American Revolution was not only a political and Freemasonic rebellion (Franklin was the top Freemason in Pennsylvania), but it was also a “banking” rebellion that tried to stop England from enslaving the Colonies through hard metal backed fiat currency or the attempt to create a National Land-Backed Bank that would be owned by England. This was simply an English attempt to steal all of the real estate in the Colonies. These attempts have not stopped even to this day and essentially the Government Self- Regulated Mortgage Electronic Registration Systems, Inc. company, or what some call the Mortgage Mafia, is still trying to steal land from Americans with the help of “warlord” bankers.

Franklin would be proud that his picture on the bill honors his own ingenious ways of defeating counterfeiting of paper currency. He developed a method of imprinting plant substance into the process that was very hard to duplicate. The watermarked picture of Franklin on the “Blue” $100 dollar bill is there as a counter measure for counterfeiting. You can only see the picture when you hold it up to the light.

So the overt picture of Franklin – the king of non-gold fiat currency remains on the side that will become worthless paper that is only backed up by debt at the Federal Reserve System who issues these fraudulent Federal Reserve Notes. This debt was created by a private corporation (FRS) through bad management and should go bankrupt while the gold side of the Blue Bill represents a Treasury Note that is backed up by gold (and silver) just like the new IMF Reserve Currencies of Russia and China. Once we drop our fictitious Federal Reserve Debt, we can compete again with respect in world currency markets.

Backed by Gold and Silver: Make U.S. Currency Great Again

It is time to face the inevitable: Fiat currency ALWAYS fails. If you are surprised by this truth, then please do some homework on all the fiat currencies that have been devised from Nero’s devaluing of the denarius, to Jekyll Island and creation of the Fed, to Richard Nixon and the complete severing of the dollar to the gold standard. You only think the U.S. fiat currency is safe because it has been propped up so many times during your life time. But it will fail and the end is here.Money creation via quantitative easing only leads to inflation; bailing out banks only puts more money into the market which also leads to inflation. We have reached the point now where our money holds such little value that the Federal Reserve can’t even give itself income (interest rates) off the money it prints. This is why Janet Yellen can’t raise rates.

The Federal Reserve System was created by the Congress to provide the nation with a safer, more flexible, and more stable monetary and financial system. If it were doing its job, it would “call in” the oversupply of money by increasing interest rates. But they won’t do this because their globalist big-corporate-buddies, who they really serve, would be in a world of hurt. Their cost of business would go up and so would consumer prices. That, in turn, would slow down consumer spending and cause industry to stall. Banks would also be impacted in this call-back-the-money strategy as fewer loans would be made as consumers might not buy houses and cars, and businesses would not need commercial loans to expand their operations since consumer spending would be reduced.

If the Fed had been doing its job, it would not have printed money at a pace to create an oversupply of money in the global market. A limited audit of the Fed after the 2008 financial crisis revealed that between 2007 and 2008 the Federal Reserve loaned over $16 trillion — more than four times the annual budget of the United States — to foreign central banks and globalist private companies.

There are two ways out of the Ponzi scheme of all time: a total collapse or a controlled demolition.

When we pick up the pieces of the failed fiat system, we will be smarter and wiser and choose a better course of running our economy:

- We will eliminate the Federal Reserve or it will eliminate itself by declaring bankruptcy. Since the Fed is a private corporation in the business of “making money” (literally), they can go bankrupt as any company can that overproduces and undersells its goods and services.

- For entities holding old FRNs after the collapse, please see the Federal Reserve to settle your notes. Of course, Central Banks can continue paying the debt service by printing “old currency” backed by the bankrupt Fed. All money loaned out by the Fed will have to see the Fed for redemption. Don’t come looking for We the People to bail you out this time. We did not authorize these loans and we are much more awake than we were in 2001 and 2008.

- In the meantime, the States of America and We the People will institute a new paper and digital currency based upon a gold-silver standard. These notes and digits will be controlled by the U. S. Treasury who will be prohibited from ever turning its power over to a non-governmental agency.

- We the People will be able to use a wide array of currencies—from local and state currencies, backed by the silver-gold standard—to silver coins to digital pay or bitcoin. Our U.S. Treasury issued paper and coin money supply will be backed with silver-gold just like the images we now see on the right side of the new $100 bill. We will see state banking emerge and small local banks and credit unions thrive.

I Paid off my Mortgage so Where is my Title?

In the mid-2000s, the Anonymous Patriots saw the Ponzi scheme on Wall Street and cashed in. We decided to use our proceeds to pay down our commercial buildings and residence. It was just simple math. Why pay the bank an interest rate higher than the overall return made in our portfolio? We would just invest in ourselves and keep the money. First the house was paid down and then the commercial properties, one by one. Over the last few years, we have become free of the banks and keep the money that we once paid the banks to service our debt. We also diversified our cash holdings into local banks and credit unions. (We are not financial advisors so by law we cannot and will not give you financial advice. Do your own homework. Do what seems right for your household.)Why this is of particular interest in this article is that as the properties were paid off, we would ask the bank for our property titles. We kept being told that “we don’t issue property titles anymore” or “the proof of your ownership is now established with your local property tax authorities.” But this was odd since we have auto titles in our possession. Friends with boats and mobile homes have paper titles.

So what happened to property titles? We paid off our home and buildings—but do we really own them when we don’t have a paper legal title? What did the banks do with the original title and why don’t they return them to us now that the property is paid-in-full? Do you have the title to your residence or have you ever seen it? If you closed on a home since 2008 have you seen any paper titles at closing? Why aren’t title companies and banks concerned about paper titles anymore?

What we found out will shock you.

But before we get there, we want to show you one more thing about the new $100 bill that gave us a clue of what happened to residential and/or commercial property titles.Strange Image on the New One-Hundred-Dollar Bills

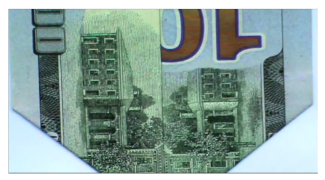

Many people have discovered the image of the twin towers collapsing on their 5, 10, 20, 50, and (old) 100 dollar bills. If you haven’t seen how these images are made by folding the bills, check out this video. There are several on the internet, but this one shows the images in all of the bills in a way that you can visualize the succession of the falling of the World Trade Center: Twin Towers Falling on Currency Bills. These images were designed on the bills long before 9-11-2001.We were curious what would image would show if we folded a new $100 bill in the same manner. This is what we found, taken from the 2009 series of the new bill, which predates the event that we will describe below, but seems to be a prophetic warning nonetheless:

We see what seems to be a rush of water down a street, from an open source of water, into an urban area. This is what we began to search on the internet. Had there been any floods in urban areas that might have currency consequences?

Flood-Fire-Flood on Water Street, NYC, 2009

About 40 trillion worth of stock and bond certificates held in an underground Manhattan vault owned by the Depository Trust & Clearing Corporation were damaged by flooding in Hurricane Sandy in November 2012. The New York-based company DTCC processes transactions in U.S. equities and government, municipal and corporate bonds. The 40-year-old vault was submerged when the Atlantic Ocean’s largest tropical storm on record slammed New York City.The DTCC processes the underwriting of stock and bond offerings for all transactions on the New York Stock Exchange and electronically registers securities and ensures that dividend payments are accurate. It also manages transactions and payments in equities and fixed income and guarantees that trades clear. Purchases and sales are mainly handled through electronic book entry, with the securities registered in the name of DTCC unit Cede & Co. The DTCC is owned by its member banks, brokers, mutual funds and other financial institutions.

The “Unfortunate and Unpredictable” destruction of $40 Trillion in Stocks and Bonds must have come as a shock seeing that a fifth grader wouldn’t house the largest depository of “paper” stocks and bonds in a vault below sea level and then, forget to close the door. That’s right, the vault was waterproof, but someone forgot to close the door on the way out after they heard the largest hurricane to ever hit Manhattan was on the way. But that is only topped by the fact that after the flood drained, a fire somehow burnt the contents of the vault. And then, another flood somehow filled the vault again leaving a mess that DTCC says may never be cleared up.

Coincidence?

Then we are told by DTCC that the remains of the $40 trillion paper trail has been moved to a secret location; furthermore, no pictures of the “damp and burnt” records were ever shared with the public. This is made even odder when we read from DTCC own newsletter its intentions concerning “paper” copies of anything traded on the New York Stock exchange. As a matter of fact, just prior to the 2012 flood, DTCC called for a “dematerialization” of paper copies of any transaction on the NY Stock Exchange, or any other exchange.From the site of the DTCC, September 1, 2012

Targeting Paper

DTCC Calls for Full Dematerialization

DTCC’s dematerialization plan focuses on three primary areas in physical processing: traditional physical transactions, new issues and existing inventory in the vaults of The Depository Trust Company (DTC). To target these areas, DTC will:

- Introduce ways to reduce volumes, costs and risk associated with traditional physical transactions. These are transactions clients regularly send to DTC for immobilization. DTC anticipates eliminating physical deposit activity altogether by 2015.

- Develop recommendations that will eventually eliminate the need for physical certificate processing of new issues.

- Work with the industry to reduce physical certificates held in the DTC vault, as well as reducing and ultimately eliminating those certificates held in DTC’s street name, Cede and Co. This will not affect the depository’s Non-Cede Custody Service, which offers limited services for assets that are not fully eligible.

As of September 2014, DTCC had not replaced the damaged stock certificates and had laws suites filed against it. There were also many thousands of FBI and other documents also stored in this “depository.” DTCC was not worried at all about the loss because most the of the stocks and bonds were owned by their sister partner, Cede & Co. And as we can see in their Targeting Paper above, DTCC was hoping to “dematerialize” the Cede & Co stock and bonds…then OOPS!…Someone just happened to leave the vault door open for Hurricane Sandy.

It is worth taking a moment here and delving into the mystery company DTCC and its partner in crime, Cede & Company.

DTCC and its partner in crime, Cede & Company

Wikipedia defines DTCC as: “An American post-trade financial services company providing clearing and settlement services to the financial markets. It also provides central custody of securities. DTCC was established in 1999 as a holding company to combine The Depository Trust Company (DTC) and National Securities Clearing Corporation (NSCC). User-owned and directed, it automates, centralizes, standardizes, and streamlines processes in the capital markets. Through its subsidiaries, DTCC provides clearance, settlement, and information services for equities, corporate and municipal bonds, unit investment trusts, government and mortgage-backed securities, money market instruments, and over-the-counter derivatives. It also manages transactions between mutual funds and insurance carriers and their respective investors. In 2011, DTCC settled the vast majority of securities transactions in the United States and close to $1.7 quadrillion in value worldwide, making it by far the highest financial value processor in the world.”DTCC’s depository provides custody and asset servicing for more than 3.6 million securities issues from the United States and 121 other countries and territories, valued at US $36.5 trillion. In 2010, DTCC settled nearly US $1.66 quadrillion in securities transactions in 2012.

DTCC is about 34% owned by the New York Stock Exchange on behalf of its members. It is a limited purpose trust company and is a unit of the Federal Reserve.

How are Stock and Bonds Actually Purchased

In the good old days when you bought a share of stock, it was accompanied by a paper stock certificate. Today when you make this transaction, the broker will place your stock or bond purchase into their safekeeping under a “street name.” No bank or broker can place any stock or bond into their firm’s own name due to Federal Trade Commission (FTC) and Security and Exchange Commission (SEC) regulations. The broker or bank must then send the transaction to the DTCC for ledger posting or book entry settlement under mandate by the Federal Reserve System. Remember, since your bank or broker can’t use their name on the certificate, they use a fictitious street name.Since the DTC is a banking trust company, it can’t hold the certificates in its name wither…..so the DTCC transfers the certificates to its own private holding company or nominee name. The DTCC’s private holding company or street name, is shown as either “CEDE and Company”, “Cede Company” or “Cede & Co.” After this transactional process, you, the so-called purchaser of the stocks, have no real, no actual, no legal claim over these stocks, certificates, or bonds.

Or, as one stockbroker said about the DTCC and ownership of stock: “Nobody owns stock. What you own is an entitlement to stock held for you by your broker. But your broker doesn’t own the stock either. What your broker owns is an entitlement to stock held for it by Cede & Co., which is a nominee of the Depository Trust Company, which is a company that is in the business of owning everyone’s stock for them. If I sell stock to you, I don’t have to courier over a paper share certificate, or call up the company and have it change its shareholder register. Our brokers just change some electronic entries at their DTC accounts and everything is cool.”

Mortgage Mafia Owns 80% of US Titles

Just as Cede & Co. at one point in every transaction on Wall Street “owns” the stock or bond or anything traded, so, too, the mortgage industry was taken over by similar “digital pirates” who used computer programs to eliminate paper notes or titles- kind of like fiat currency backed up by nothing. The Mortgage Electronic Registration System essentially owns 67 million pieces of property in the US at this moment, or about 80% of all US residential titles. And that explains why the Anonymous Patriots, despite paying off our properties in full, cannot get a title on our properties from the bank who held our mortgages.For those readers who made it so far, don’t think that you are an exception. Continue to read on:

When the Mortgage Electronic Registration Systems, Inc. was created, it was intended to serve as a nominee for real estate transactions in a way strongly analogous to how Cede & Co. serves as the nominee owner of record (i.e., the “street name” owner) for all securities held in trust by the Depository Trust & Clearing Corporation. In the late 1960s and early 1970s, the American securities industry was drowning in paper because of the sheer complexity of physically exchanging thousands of stock certificates every day. By “immobilizing” physical stock certificates and later replacing them altogether with book entries, DTCC enabled the development of the modern computerized securities industry.

The MERS system eRegistry is a system of record that identifies the owner (Controller) and custodian (Location) for registered eNotes. Built by MERSCORP Holdings, Inc. with the endorsement of the Mortgage Bankers Association (MBA) and launched in 2004. Both Fannie Mae and Freddie Mac require the registration of eNotes on the MERS system eRegistry before they are eligible for purchase.

As mortgage-backed securities grew in volume during the 1980s, it became self-evident that a similar mechanism was needed for the mortgages placed into those securities. MERS fixed this problem in that most standard loan documents were changed to name MERS as the nominal beneficiary or mortgagee of record. This enabled lenders and investors to transfer mortgages without recording assignments in local recorders’ offices and, in turn, avoided having to pay recording fees.

Ideally, assuming a loan is properly paid back on time, a MERS loan needs only two documents to be recorded:

1) the original mortgage or deed of trust naming Mortgage Electronic Registration Systems, Inc., and a reconveyance of the mortgage or

2) deed of trust back to the borrower (thus merging legal and equitable title).

If all entities along the way are MERSCORP Holdings, Inc. members, then all intermediate transfers between those points are tracked only on the MERS system, and the entity who holds the loan at the end merely records the reconveyance as an agent for MERSCORP Holdings, Inc. (Notice how MERS is both (1) an agent for the original lender, and then (2) the final lender acts as an agent for MERSCORP Holdings, Inc.; this is why MERS’ critics frequently attack it as “two-faced.”)

Some of the illegal activities of MERS named in the many law suits against it include:

MERS’s officers often issue assignments without verifying the underlying information, which has resulted in incorrect or fraudulent transfers.

Simultaneously claim to be the mortgagee and the nominee/agent of the lender or trustee.

Harmful effect on the integrity and transparency of public recording and tax avoidance.

Its nominal ownership of millions of home loans poses a disastrous risk for mortgage investors should Mortgage Electronic Registration Systems, Inc. ever declare bankruptcy.

MERS was used by the Wall Street Banks to avoid paying county recorder fees and real estate transfer tax fees.

Using a long list of names who are known “robo-signers.”

MERS is a shell company with no employees, owned by the giant banks.

MERS is a tax and fee-avoiding opportunity.

MERS has all but replaced the nation’s public land ownership records.

MERS placed many undiscovered and no document mortgages in circulation.

The bundling and sale of mortgages and claims of title can make it very difficult to know who owes what to whom.

For the first time in the nation’s history, there is no longer an authoritative, public record of who owns land in each county.

There is an unbelievable scandal in the making that threatens to subvert our four-century-old method for guaranteeing a fundamental building block of the American republic—property ownership.

Created in 1995 by the country’s biggest banks, MERS quietly took control of and privatized mortgage record-keeping across the country and, in the span of a few years, scrambled America’s private property ownership records to the point where no one could figure out who owns what.

MERS was a tool used by America’s top financial institutions to pump up the real estate market.

Mortgage-backed securities, robo-signers, lightning quick foreclosures, subprime mortgages and just about everything else that went into feeding the biggest real estate bubble in U.S. history could not function without help from MERS.

MERS was created to help the industry push its latest money-maker: mortgage-backed securities, a Wall Street financial scam that dressed up the most toxic, guaranteed-to-fail loans as Grade A investment vehicles that could be sold to suckers looking for an easy gain.

The whole purpose of MERS is to allow “servicers” to pretend as if they are someone else: the “owners” of the mortgage, or the real parties in interest.

MERS artifice and enterprise evolved into an “ultra-fictitious” entity, which can also be understood as a “meta-corporation.”

The average consumer, or even legal professional, can never determine who or what was or is ultimately receiving the benefits of any mortgage payments. The conspirators set about to confuse everyone as to who owned what. The use of MERS as a generic placeholder for the real owner of a mortgage was a crucial component of the entire securitization machine. The entire scheme was predicated upon the fraudulent designation of MERS as the ‘beneficiary’ under millions of deeds of trust.

Before MERS, it would not have been possible for mortgages with no market value to be sold at a profit or collateralized and sold as mortgage-backed securities. Before MERS, it would not have been possible for the Defendant banks and AIG to conceal from government regulators the extent of risk of financial losses those entities faced from the predatory origination of residential loans and the fraudulent re-sale and securitization of those otherwise non-marketable loans.

From 1997—the year MERS went online—to 2005, mortgage fraud reports increased by 1,411 percent. MERS saved the banking industry—and cost municipal governments—tens of billions of dollars by allowing lenders to avoid paying county filing fees. MERS extracted at minimum around $30 billion from cash-strapped local governments.

MERS also has almost no paid employees and does not keep any records or minutes of corporate meetings. When pressed to explain the inner workings of the organization, its executives evaded questions, feigned ignorance.

In California, the suit against MERS could cost the company somewhere between $60 to $120 billion in damages and penalties.

Almost every participating major bank in MERS has been charged for mortgage fraud and paid fines in the billions.

How Did MERS Take Control

MERSCORP Holding Inc., publicly known as its shell company “MERS,” is the premier real estate mortgage holding mill and third party deed counterfeiting house in the country. After the Glass-Steagall Act, which made it a felony to speculate with mortgage notes in the stock market, was repealed by the Gramm-Leach-Bliley Act in 1999 MERS took off like a rocket. Mortgage paper was leveraged dozens of times bundled and sold to speculators. Not with hopes of gain through real estate value appreciation, but as betting chips in a game based on when properties they held would go into default; a decadent Wall Street derivative game called “credit default swaps.”The resulting global bank windfall, in stark contrast to individuals and companies both domestic and foreign, who lost big-time on these credit default swaps, and were forced to search out and attempt foreclosure on at-risk properties (whether in default or not) in order to recoup their losses and stay in the game.

The huge derivatives bubble created by the banks has created over 70 million MERS tainted properties in the US alone.

After deregulation (the Glass-Steagall repeal) the mortgage note, and the lien document were allowed to be separated. The seller would keep the lien and the note was sold to the bank for consideration which the bank then sold into a Wall Street derivative pool. There it was leveraged and resold over and over again. There are literally hundreds of court cases from 17th century English case law to today’s US Supreme Court that have ruled this practice of unrecorded title transfer as predatory and unlawful.

The Note is the signed negotiable instrument, you executed to obtain the money you borrowed. For this reason payment is due only to the lawful holder of this NOTE or to an agent who can prove he lawfully represents the owner of the actual Note and not just a copy of it. By the same token, the lien holder, has no claim to the property without possession of the actual Note.

Any mortgage company that demands payment on any property, cannot secure and lawfully receive payment nor can they foreclose and lawfully take the property with merely a copy of the mortgage Note. Any foreclosure without both the Lien and the original Note is theft.

The solution is to hold the mortgage bankers’ feet to the fire. Never let them take your property — possession is 9/10ths of the LAW. Arm yourself with the facts and make them prove their ownership in court. If they can’t prove they are the mortgage owner by producing absolute proof of the legally obtained original Note signed by you in blue ink, don’t pay them a penny and don’t let them take your property. They must be the legal holder of your Note and Lien to lawfully do so.

DTCC and Cede & Co plus MERS Have Same Owner

It would be beyond the scope of this article to explain who is the Master pulling the puppet strings of the DTCC and MERS truly is. This puppet Master essentially owns every stock exchange and every transaction that happens on those exchanges as well as most of the mortgages in the country.The move to digitalize all stocks and mortgages is similar to going from gold backed fiat currency to currency backed by digital impulses in the servers of meta-corporations which are monopolies.

Would you be surprised to know that the same company that owns the New York Stock Exchange also owns the Chicago Mercantile Exchange and most other national and international exchanges? Surely you would not be surprised to find out that the same transnational private corporation also owns DTCC and Cede & Co. and MERS. It sounds like checkmate, doesn’t it? But in coming articles we will reveal the name of this “most powerful” corporation and the evil web it spins.

Back to that Strange Image on the New One-Hundred-Dollar Bills

As we have written in other articles, we believe that there are two factions in this war of Globalism vs Nationalism. The Globalists do not want you to know that there are Patriots giving them a run-for-their-money. Literally. Thanks to the Patriots who saw what the DTCC would have to do to hide their crime after the 2008 housing collapse—a hurricane flood on a street named Water. They put their message of prophecy to us on the new currency designed in 2009 to predict what would later happen in 2012, while at the same time sneaking a new gold-back currency into the market.They also included a very important message to all of us on the new currency. We The People, by the stroke of a pen and the will of the people, can determine the outcome of this war. Let Patriots around the country consider the following actions:

- Exchange old currency for the new, either by a direct exchange at the banks or using up the old currency in paying bills, etc.

- Stop playing their mortgage game and demand to see your paper title when you feel it is right for your personal situation—either by refusing to pay your mortgage until you see proof of the title, demanding proof at the time of remortgaging, or other suggestions given to us by legal and financial Patriots.

Until then, don’t take any wooden nickels, old Federal Reserve Notes and remember to demand paper copies of all titles, notes, liens, stocks and bonds. Until then, keep holding on to those Blue bills. And when we have a favorable political situation in Washington, we must demand, by Constitutional Amendment or rock-solid legislation, the complete cessation of the DIGITALIZATION of our money, stocks and bonds, and LAND of the citizenry.

Thanks to: http://www.cosmiconvergence.com